What is a Certificate of Insurance? A Guide for Home Inspectors

Last Updated November 9, 2023

Pretend you’re a home inspector who has just been asked to inspect a newly built, single-family home. As you prepare for the inspection, you get an email from the builder requesting that you send them a copy of your certificate of insurance.

You may wonder: What is a certificate of insurance? Does it cost money? Is it hard to get? Does sharing my insurance information with the builder put me at risk?

Here at InspectorPro, we get those questions all the time. We figure it’s time to familiarize you with this useful document so you’ll never need to ask “What is a certificate of insurance” again. Better yet, you’ll be prepared anytime a builder or client requests one.

What is a certificate of insurance?

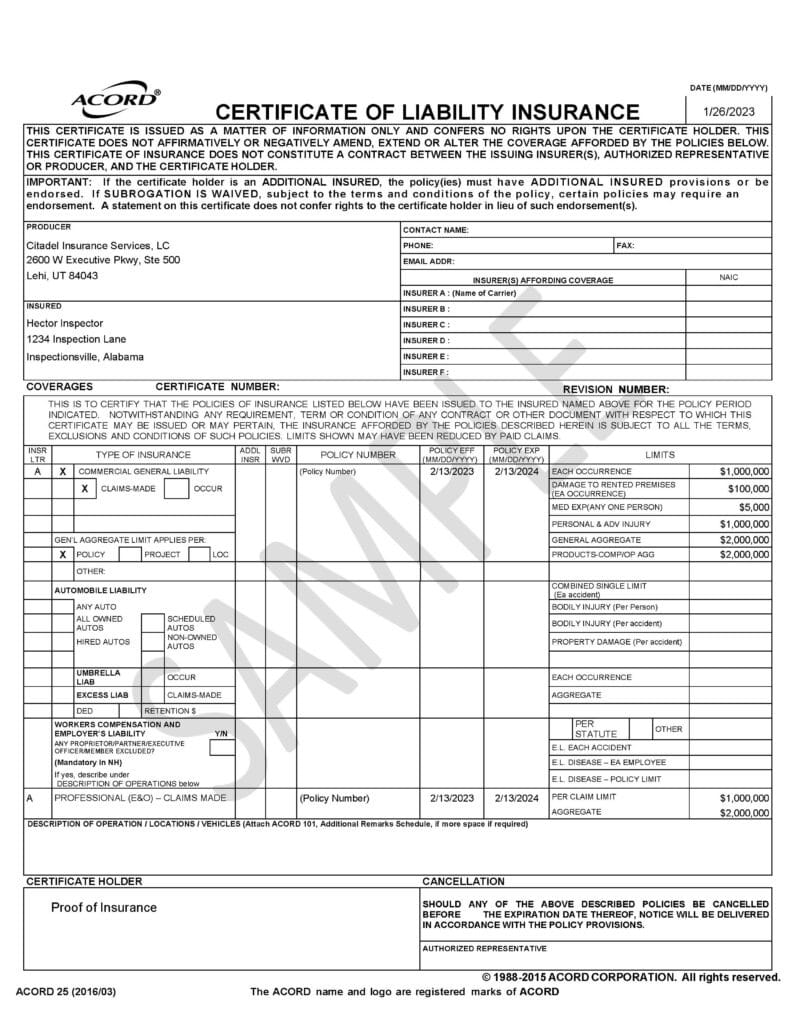

Also known as proof of insurance (POI), a certificate of insurance (COI) is a written document that proves you currently carry insurance.

What does a certificate of insurance contain? While not all COIs look the same, they often contain similar information, including:

- Your name and address

- Your business or DBA name and address

- A simple breakdown of your coverage and limits (i.e., $1,000,000 of commercial general liability or errors and omissions coverage)

- The names of employees covered under the policy

- The certificate holder or entity to whom you’re providing the certificate

Here is a certificate of insurance example:

Most of the information listed above is in the declarations, or dec page, of your policy. However, while your declarations are meant for you, a certificate of insurance is meant for others. It’s also condensed into a simpler format with less information than you would find in your policy documents for both convenience and privacy.

When do you need a certificate of insurance?

When a client wants to confirm that you have the insurance coverage to respond to any claims or damages caused by your inspection, they will ask for a certificate of insurance. It will often be builders, realtors, franchisors, and larger commercial clients who need COIs before you can inspect a property. Also, state governments may require proof that you meet the minimum insurance requirements before you can get your license as a home inspector.

When you are inspecting a new build, for example, the builders are concerned that you’ll break or cause damage to their newly finished property. So, they want to make sure you can cover anything that you break with commercial general liability insurance. (If you’re curious about the top five general liability claims made against home inspectors, read here).

For commercial clients, they may wish to see proof of errors and omissions (E&O) insurance to cover any issues that you may have missed, since commercial inspection mistakes can lead to large claims. After all, the claimant may drag your client into the claim due to your alleged negligence.

If clients are particularly concerned about being named in claims for your alleged mistakes or accidents, they may go a step beyond asking for a COI and request you add them as an additional insured to your insurance policy. Doing so would allow your policy to cover them. For more information on additional insured endorsements, read this article.

If your client hasn’t requested a certificate of insurance, do you need to send one? No. In fact, if they haven’t asked for it and you send one anyway, you may introduce the idea of getting reimbursed for any issues they find, which can lead to unnecessary claims.

How do you get a certificate of insurance?

While it may sometimes feel like your clients are asking you to jump through hoops for a COI, many insurers make the process simple. In fact, most insurance providers send a copy of your certificate of insurance when you bind coverage or renew your policy. If you save that copy in your policy, it’s often sufficient for clients.

On the other hand, if clients request an additional change, such as their name in the certificate holder space, or that you add them as an additional insured, or any other special wording, just contact your insurance provider. Your broker and their account manager deal with many COI requests throughout the day. So even if you don’t understand the specifics of your clients’ demands, your provider can help clarify for you and send you the certificate of insurance with any needed changes.

When you request a certificate, give your insurance provider the following information:

- Your name

- The name of the client (i.e., the builder)

- The client’s office address

- Any special instructions

Then, your provider will confirm that you’re carrying sufficient coverage to meet your client’s certificate of insurance requirements and send you the COI. If your client is requesting different coverage or greater insurance limits than you currently have, your provider can help you. This may mean you need to increase your coverage, even mid-policy, to meet their requirements. Simple, right?

Your insurer can only write a certificate of insurance showing coverage that they provide for you. This means that you may need to request multiple COIs in the case that a client requests proof of insurance for multiple coverage types that you carry through multiple insurers.

Be prepared when a client requires proof.

A certificate of insurance request from a client is not something to stress out about. Or, it doesn’t have to be if you carry the correct coverage and have an insurer who prioritizes client support. InspectorPro is grateful to provide quick responses to and client education about certificates of insurance.

If you would like an experienced home inspector insurance provider to have your back, contact us for a quote.

We look forward to helping you jump through as many hoops as you need to so that you can become a successful inspection business.